Will Bitcoin ETFs follow gold ETFs’ path to success?

Will the much-anticipated approval of spot Bitcoin ETFs be the catalyst for widespread adoption, or could it paradoxically hinder Bitcoin’s growth?

As of Dec. 11, the U.S. Securities and Exchange Commission (SEC) has not approved any spot Bitcoin (BTC) ETF applications despite growing interest and numerous filings from major financial entities.

This persistent reluctance stems from concerns about fraud and market manipulation, with the SEC emphasizing the need for a “comprehensive surveillance-sharing agreement with a regulated market of significant size.”

Historically, applications for Bitcoin spot ETFs have been repeatedly submitted and rejected. Notable investment firms like Ark Invest, Invesco, WisdomTree, VanEck, Bitwise, and Valkyrie have all faced rejections in their attempts to launch such products.

Despite these setbacks, the race for approval continues, with BlackRock, the world’s largest asset manager, recently filing a renewed ETF application. This move has sparked renewed hope in the crypto community, considering BlackRock’s successful track record with ETF applications.

But what does history tell us? Looking back at the gold market’s evolution post-ETFs, we see a path paved with increased demand and soaring prices – a path Bitcoin might well follow.

Yet, Bitcoin, with its unique digital nature and a market dynamic distinct from traditional assets like gold, presents a complex and multifaceted scenario.

Let’s delve into this intricate narrative, exploring the historical parallels, expert opinions, and economic implications of a world where Bitcoin spot ETFs are no longer a hypothetical but a reality. How will this impact Bitcoin’s trajectory, and what does it mean for investors, idealists, and the global financial landscape?

Gold vs Bitcoin: what does history tell us?

The history of gold ETFs offers valuable insights into how a potential approval of a Bitcoin spot ETF could impact the cryptocurrency’s market dynamics.

The first gold ETF, Gold Bullion Securities, was launched on the Australian Securities Exchange in March 2003, followed by the launch of SPDR Gold Shares (GLD) in the United States in November 2004. This marked a significant shift in how investors could access the gold market.

Before the advent of gold ETFs, investment in gold was typically done through physical gold purchases or shares in gold miners, which offered leverage to gold prices.

Physical gold, however, had several drawbacks, such as sales tax, storage costs, and regulatory constraints, making it less accessible to the average investor.

The introduction of gold ETFs democratized gold investment, offering a more straightforward and cost-effective way to invest in gold without owning it physically. This ease of access played a pivotal role in increasing gold’s appeal to a broader range of investors.

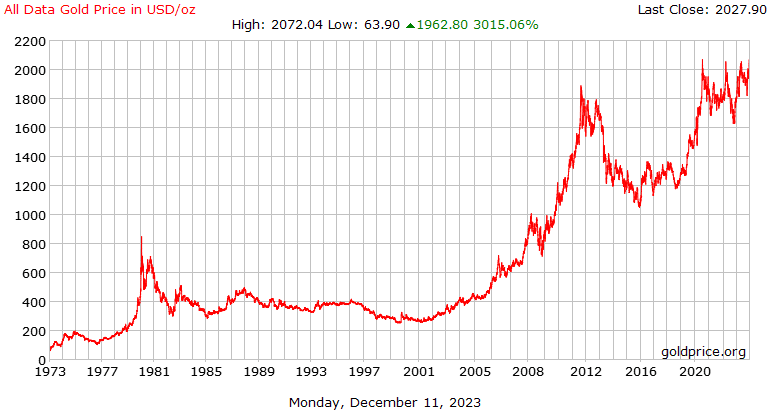

The impact of gold ETFs on the market was substantial. The gold price, which had been in decline from its peak in 1980, began to rise steadily after central bank selling stopped and VAT was removed on physical gold purchases.

Following the launch of the first gold ETF, gold prices experienced a significant increase. Between 2004 and 2011, gold price soared from around $450 to more than $1,820, marking a nearly 350% increase.

Drawing parallels to Bitcoin, the approval of a Bitcoin spot ETF could potentially have a similarly transformative effect.

A Bitcoin spot ETF would provide direct exposure to Bitcoin’s price, making it more accessible to a wider range of investors, including those less inclined to navigate the complexities of cryptocurrency exchanges or digital wallets.

This increased accessibility could lead to higher demand and potentially drive up Bitcoin’s price.

However, it’s crucial to consider the differences between gold and Bitcoin markets. Bitcoin’s market dynamics, regulatory environment, and investor profile differ significantly from those of gold. While history can provide insights, the impact of a Bitcoin spot ETF could manifest differently due to these unique factors.

What do experts think?

Nitin Gaur, Global Head of Digital Asset and Technology Design at State Street, opines that Bitcoin ETFs could usher in a transformative era for Bitcoin’s market dynamics. He says:

“The approval of Bitcoin ETFs is not just a regulatory milestone; it’s a gateway to unprecedented capital inflows into the Bitcoin ecosystem. Post-approval of these spot Bitcoin ETFs, we could witness Bitcoin’s price soaring past $60k levels by the next halving event.”

Gaur also emphasized the broader implications beyond the price jumps, focusing on how Bitcoin spot ETFs could fundamentally alter Bitcoin’s long-term viability and acceptance in the financial ecosystem. He further mentioned:

“This isn’t merely about price increments; it’s about legitimizing Bitcoin in the eyes of traditional investors and accelerating its journey to becoming a mainstream financial asset.”

Meanwhile, Hubertus Hofkirchner, founder of Bitcredit Protocol, offered a nuanced perspective on the potential impact of Bitcoin spot ETFs.

“The excitement around ETF approval embodies the dichotomy within the Bitcoin community — idealists championing a new monetary paradigm, and investors eyeing price appreciation. While an ETF could indeed propel Bitcoin’s value due to increased scarcity, idealists worry about amplified volatility undermining Bitcoin’s adoption in the real economy.”

Hubertus Hofkirchner, Founder of Bitcredit Protocol

These concerns center around the potential for heightened volatility, which could deter Bitcoin’s adoption in everyday transactions and its acceptance as a stable financial instrument in the broader economy. This volatility, fueled by speculative trading often associated with ETFs, could undermine the very attributes—such as stability and reliability—that make Bitcoin an attractive alternative to traditional currencies.

He also pointed out the contrast between Bitcoin and traditional commodities like gold, noting that Bitcoin’s unique digital attributes differentiate it significantly from physical commodities:

“Unlike gold, Bitcoin’s digital nature eliminates the logistical challenges of physical commodities, which might render the allure of a Bitcoin ETF less compelling than it was for gold.”

Consequently, the primary appeal of a Bitcoin ETF lies not in addressing logistical challenges, as with gold, but rather in offering a regulated, mainstream financial instrument for Bitcoin investment.

Turning to a critical viewpoint, Peter Schiff, a well-known skeptic of cryptocurrencies, offered a starkly different take in his recent tweet.

Schiff’s perspective embodies the skepticism some traditional investors hold regarding the sustainability and real value of Bitcoin, especially in comparison to traditional assets like gold.

Hence, while some Bitcoin ETFs are a game-changer that could significantly boost Bitcoin’s value and mainstream appeal, others caution about potential volatility and the contrast with traditional assets.

Unraveling the economic implications of Bitcoin spot ETFs

While crypto enthusiasts are excited about the introduction of Bitcoin spot ETFs, believing it could increase Bitcoin’s price, it’s essential to distinguish between price and value.

The ease of trading an ETF could indeed attract new demand from those who find owning Bitcoin directly cumbersome, potentially raising its price in the near term. However, this does not inherently improve Bitcoin’s underlying value.

From an economic standpoint, the concept of a “negative sum game” is crucial in understanding the potential impact of Bitcoin ETFs.

In game theory, a zero-sum game is a situation where one participant’s gain or loss is exactly balanced by the losses or gains of other participants.

Bitcoin, when viewed through the lens of trading and investment, can be likened to a negative sum game, similar to poker in a casino with a rake. Here, the winner’s gain equals the sum of losses from other players, but additional costs (the “rake”), like trading commissions, margin interest, and promotional expenses, create a net loss in the system.

The introduction of ETFs potentially increases this “rake”. While it might streamline access to Bitcoin, the additional layers of fees and expenses associated with ETFs could exacerbate the negative sum nature of the investment.

This is particularly relevant if the ETF structure does not add intrinsic value to Bitcoin but merely offers a more convenient investment vehicle. In such a market, only highly skilled traders (similar to professional gamblers) might profit, primarily during times of high influx of inexperienced traders. However, this is not sustainable.

As less experienced traders exit the market after losses, the competition among skilled traders intensifies, making it harder to overcome the increased costs and maintain profitability.

Moreover, the introduction of Bitcoin ETFs could impact Bitcoin’s decentralization ethos. While ETFs might bring Bitcoin closer to mainstream financial systems and increase its adoption, they do so by integrating it within traditional financial structures, which may be contrary to the original decentralized, anti-establishment vision of Bitcoin.

In conclusion, while Bitcoin spot ETFs might increase the cryptocurrency’s price and mainstream appeal in the short term, they introduce complexities that could affect its long-term economic sustainability and philosophical ethos.

The differentiation between price increase and true value addition is critical in assessing the potential impact of these financial instruments on Bitcoin’s market dynamics.