Investors prefer ‘breakout trends’ over ‘moonshots’ and that’s a problem, VC says

There are fewer crypto investments nowadays, according to venture capitalist Adam Cochran.

VCs often face pressure from their limited partners who are primarily focused on beating index fund returns.

Cochran — founder of the firm CEHV — explained in a thread on X.com: “VCs have slowed investing in crypto by a lot, and [it’s] a bit of a nuanced reason: 1. Most of them have LPs that just want to beat index fund returns. 2. Over a medium term the [risk/return ration] of owning Bitcoin and ETH will easily beat index funds, and can only be beat by early stage bets.”

See below.

VCs often target high-growth startups and emerging technologies that offer substantial upside potential.

For instance, the S&P 500 index fund, a common benchmark for U.S. equities, has delivered an average annual return of approximately 15% over the last five years, according to data from curvo.eu.

In contrast, Bitcoin (BTC) has largely outperformed index funds over the same period, garnering about 45% in average annual returns.

Cochran — a specialist in fintech, artificial intelligence and cryptocurrency — highlighted that even though crypto investments harbor high risks, they have historically outperformed index funds over the medium term, presenting high-reward opportunities. However, he added that VC funds are usually skeptical about making such investments at the early stage due to the risk factor of digital currencies.

The venture capitalist explained that many VCs opt to hold investments in Bitcoin and Ethereum (ETH), along with a few high-profile breakout projects, to generate fees and return capital.

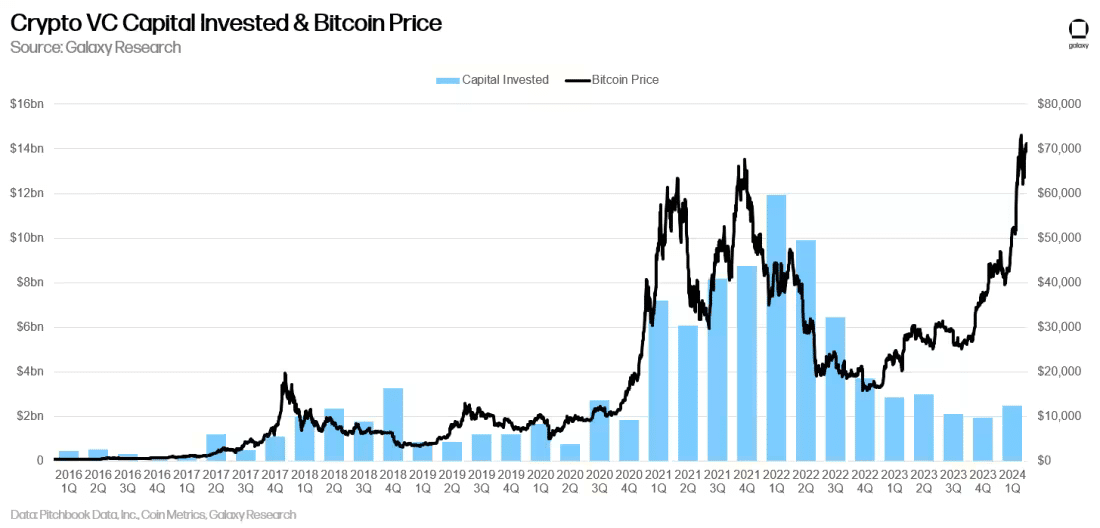

Per a recent study from Galaxy Research, in the first quarter of 2024, approximately 80% of venture capital funding was allocated to early-stage companies, with the remaining 20% going to later-stage firms.

Despite a decrease in interest from large generalist VC firms, which have either exited the crypto sector or significantly reduced their investments, crypto-focused early-stage venture funds have remained active.

Many of these funds still have capital from their 2021 and 2022 fundraises, allowing promising early-stage crypto startups to secure funding. However, later-stage startups face increased difficulty in raising capital due to the reduced involvement of larger VC players.

According to Cochran, during the last market cycle, VCs were more active in investing in applications that had already gained traction, such as OpenSea, hoping to capitalize on late-stage consumer growth.

Moreover, he believes that with interest in previous trends like non-fungible tokens, or NFTs, as well as AMM forks, DeFi, and layer 2 solutions cooling down and the market awaits the next big innovation, VC firms are in a holding pattern.

Cochran noted that while some builders continue to develop new ideas without external capital, discovering the next major trend is stalled.

This situation is exacerbated because VCs believe idle capital can earn substantial returns in money markets, discouraging early-stage investments.

He added that this period of inactivity serves as a litmus test for VC firms’ genuine commitment to the crypto industry.

Those with a deep understanding of the space can still make impactful early-stage investments. In contrast, others may only invest in later-stage opportunities, revealing a lack of true alignment with the sector.