How can I open a Bitcoin account?

Bitcoin is the most popular cryptocurrency worldwide. In this article, we provide straightforward guidance on how to purchase the currency.

Information current as of April 2024.

If you’re looking to dip your toes into the world of digital assets, understanding how you can open a Bitcoin (BTC) account is a good first step. Whether you’re intrigued by the promise of decentralization, financial autonomy, or the mechanics of digital currency, this guide aims to demystify the process and empower you to embark on your journey into the realm of Bitcoin.

Theoretically, opening a Bitcoin account can be as easy as installing an app on your mobile device or laptop. However, just because BTC can be stored digitally doesn’t mean you should keep it just anywhere. If you are planning to open a bitcoin account, this guide will tell you much of what you need to know.

Table of Contents

What is a Bitcoin wallet?

Wallets that store Bitcoin can typically store cryptocurrency holdings like Ethereum (ETH) and Ripple (XRP). This digital storage device contains private keys to access and spend your coins. They come in many forms, including physical hardware devices, software applications, and even paper printouts. You can use your Bitcoin wallet to send and receive payments and store funds securely offline in so-called cold storage.

Most Bitcoin wallets put you in control of your private keys, meaning you are responsible for keeping your bitcoins secure. Depending on how diligent you are about using your private keys, this can be advantageous or disadvantageous.

How does a Bitcoin wallet work?

Just like you need a physical wallet to store your cash and credit cards, a Bitcoin wallet stores your BTC. However, a Bitcoin wallet is entirely digital and functions like an email address.

Users must log into their account using their private key, access crypto, and send amounts to the intended recipients.

There are two main types of bitcoin wallets:

- Hot wallet: These store Bitcoin private keys on internet-connected devices. While they are convenient and easy to use, they can pose a significant security risk to bitcoin holders who lose their primary device. As a result they may be best used to store small amounts of crypto.

- Cold wallet: These store bitcoin private keys offline. They are highly secure and with a far smaller risk of compromise by hackers.

How to open a Bitcoin account: step-by-step

Now that you know the basics of Bitcoin, let’s explore a simple step-by-step process of how to open a BTC account.

- Research. Take some time to thoroughly research the different kinds of exchange websites that support Bitcoin and what they offer, such as Coinbase, Kraken, or Bitstamp. This will help you determine which is the most suitable for your needs.

- Registration. Go to the cryptocurrency exchange website that you have chosen. Enter your email address and a strong password. You’ll receive a verification code in your email.

- Verification. Exchange platforms typically have Know Your Customer (KYC) and Anti-Money Laundering (AML) that require users to verify their address by submitting documents such as ID. This process can vary from minutes to days depending on the exchange’s requirements and the number of verifications they need to complete.

- Deposition. Once you verify your account, you can start depositing funds immediately. There are many ways to transfer funds, including bank transfers and credit cards. However, users should ensure they look into the processing time and fees associated with each method of deposition, as they may vary from one exchange to another.

- Buying and selling crypto. Once you’ve deposited your funds, you can buy and sell bitcoin.

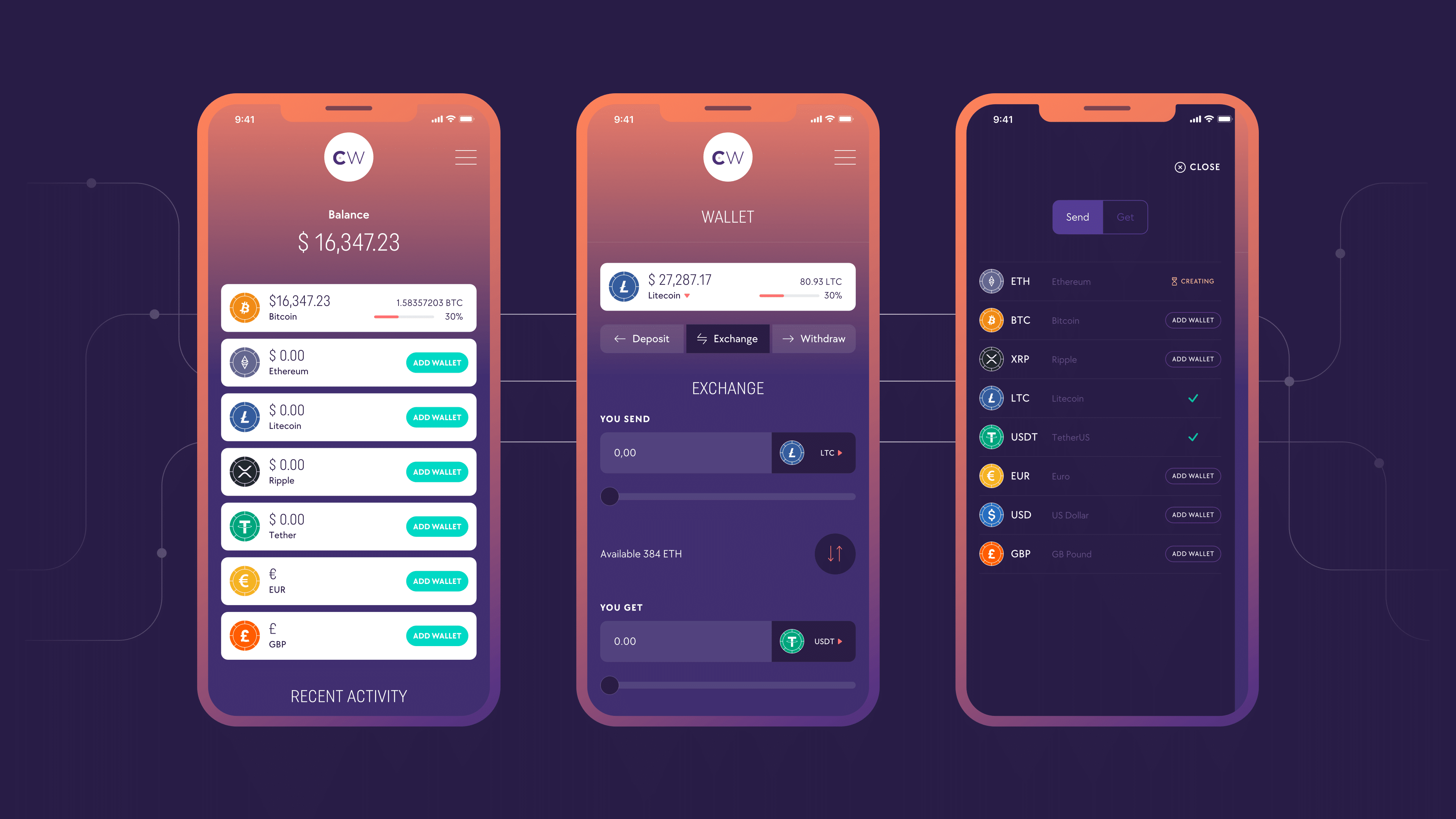

Types of wallets

Not unlike physical wallets, there are many Bitcoin wallets to choose from, each with their own advantages and disadvantages.

Mobile wallet

A mobile crypto wallet is perfect for face-to-face trades and shopping at brick-and-mortar establishments. Most mobile wallets use near-field communication (NFC), allowing users to tap their phone on a terminal to start a transaction.

Pros

- Highly portable and convenient.

- Easy to set up.

- Added security with two-factor authentication.

Cons

- May be more prone to hacking compared to cold wallets.

- May offer users reduced control over nodes and transactions.

One example of a mobile wallet with an exchange service incorporated is EU-licensed CryptoWallet. Within the app, you can create multiple wallets for bitcoin, ether and other cryptocurrencies. Like many mobile wallets, it allows customers to pay online and spend crypto like real money. CryptoWallet also offers an affiliate program. When your associate registers in CryptoWallet using your rewards code, you’ll get a percentage of any transaction fees charged.

Trust Wallet is a popular mobile wallet integrated with crypto exchange Coinbase. Like CryptoWallet, it allows users to store multiple cryptocurrencies and even NFT collectibles in one place. The wallet is integrated with BinancePay which allows you to use cryptocurrencies in the real world, for instance, pay in shops.

Mobile wallets are trying to keep pace with security measures and regulations. For instance, in March 2023 CryptoWallet renewed a trading license in Estonia amid tightening EU crypto legislation. However, it’s worth remembering all the cons mentioned above and consider avoiding storing big amounts of crypto in hot wallets.

Software wallet

Software wallets are mobile or desktop applications that connect to the internet to facilitate transactions. Most software wallets are fully self-custodial, meaning wallet providers cannot access your cryptocurrency – only you can.

Pros

- No cost to download, no registration fee.

- Easy to use.

Cons

- Dependence on electronic devices.

- Potential for user error.

MetaMask is probably one of the most popular software wallets, with a browser extension and an app available to users. As a software wallet, it provides a convenient way to store, send, and receive ethereum and ethereum-based tokens like ERC-20 and ERC-721.

Integration with dapps is one of the MetaMask advantages. It seamlessly integrates with multiple dapps, enabling users to access various decentralized services, like decentralized exchanges (DEXs), lending platforms, and gaming applications.

Users can easily add custom tokens to their wallets, enabling the management of a wide range of assets. However, MetaMask supports only ethereum-based tokens, making it unsuitable for users seeking a multi-chain wallet solution.

It is also important to keep in mind the cons of using software wallets. For instance, it may not be decentralized enough for some crypto enthusiasts, as MetaMask transactions are publicly visible on the blockchain, which could reveal users’ wallet addresses and associated transaction history.

Moreover, although MetaMask offers reasonable security features, it does not provide the same level of protection as hardware wallets, which are considered the most secure way to store crypto assets.

Hardware wallet

Hardware wallets are cold wallets that can perform offline transactions. There are several different types of hardware wallets available on the market. The most popular ones are the Ledger Nano S and Trezor Model T. These wallets support a wide range of cryptocurrencies and have built-in screens that make it easy to confirm transactions before signing them.

Pros

- Keys are more secure as they are never connected to the internet.

- Easy to back up and restore.

Cons

- Not ideal for frequent bitcoin transactions as they can be difficult to access.

- Some hardware wallet sellers are unreliable/not secure.

Centralized exchange wallet (CEX)

CEXs are similar to trading accounts in that third parties manage accounts, exchanges, wallets, and transactions.

Pros

- Easy to set up and use

- Compatible with desktops or mobile devices

Cons

- Stored Bitcoin may be at risk of hacking or operational faiures

- Requires permission for withdrawal

- Longer withdrawal periods

- Higher transaction fees compared to non-custodial options

Binance’s peer-to-peer (P2P) service can serve as an example of a centralized exchange wallet, where traders’ funds can be exchanged online within seconds. Crypto assets traded on Binance P2P are not stored on the platform itself. Once a trade is completed, the purchased crypto is transferred to the user’s Binance wallet.

Paper wallet

To use paper wallets, you must download a software package to generate key pairs. Then, you’ll print these key pairs on paper, enabling you to access and store bitcoin offline. However, over the years these kinds of wallet have become less and less prevalent among crypto users as digital wallets are considered more user friendly.

Pros

- Low-cost alternative to hardware wallets

- Ideal for face-to-face transactions

Cons

- Easy to lose paper keys

- Requires physical access to the printed keys

- Complex setup process compared to digital wallets

Conclusion

While figuring out how to create a Bitcoin account is relatively straightforward, the type of wallet you choose will dictate how secure your coins are. Think about how you want to access your bitcoin, what you want to use it for, and what is most convenient for you. Here’s the brief summary to guide you:

Hot wallets can be used for trading, paying in crypto, exchanging on P2P, and other goals that require quick access to your coins via internet. Cold wallets can be used for long-term storage of crypto, savings, etc.

When you do your homework, buying and selling crypto can be a breeze. However, it’s important to remember that there is always the risk of loss when buying or selling crypto and you should always ensure to take into consideration factors such as your portfolio spread and attitude towards risk before making any financial decisions.

FAQs: how to open a bitcoin account

Can I open a Bitcoin account on my phone?

Yes, you can open a Bitcoin account using your mobile device, especially if opening a mobile wallet. You can also open a Bitcoin account on your tablet.

Do I need to pay to open a Bitcoin account?

No, you don’t have to pay to open a Bitcoin account. However, some wallets will require that you deposit a minimum amount.

What is the best Bitcoin wallet?

Many Bitcoin wallet types suit different needs. If you prefer to transact offline, hardware or paper wallets may be most appropriate. Alternatively, an online wallet might be better if you prefer online trading.

How much is 1 bitcoin in US dollars?

Check out the crypto.news price page to find out the current price of BTC, as it’s very volatile and can change quickly.