The rise of CBDCs is inevitable but not risk-free | Opinion

To make central bank digital currencies successful, global and local financial institutions need to invest in digital currency education, analyze various use cases, and create their digital currency strategy.

Disclosure: The views and opinions expressed here belong solely to the author and do not represent the views and opinions of crypto.news’ editorial.

As cryptocurrencies like Bitcoin (BTC) continue to enter the mainstream and encapsulate people, several countries have announced initiatives to create their own central bank digital currencies (CBDCs). According to the International Monetary Fund (IMF), nearly 100 countries are actively evaluating CBCDs, and some have already started to roll out these initiatives.

CBDC Tracker | Source: Atlantic Council

Additionally, central banks worldwide are investigating the practicalities of establishing CBDCs of their own. Digital currencies are surging in popularity for a variety of reasons. They are considered more secure and less volatile than cryptocurrency assets. Some also feel CBCDs could improve the safety and efficiency of payment systems.

It is also believed that CBCDs can help promote financial inclusion across the world, particularly in areas with limited access to financial services. Additionally, CBDCs are not a new concept; they have been around for three decades. However, it wasn’t until recent years that research in CBDCs proliferated globally. This was largely due to the decline in the use of physical cash transactions, but also technological advances.

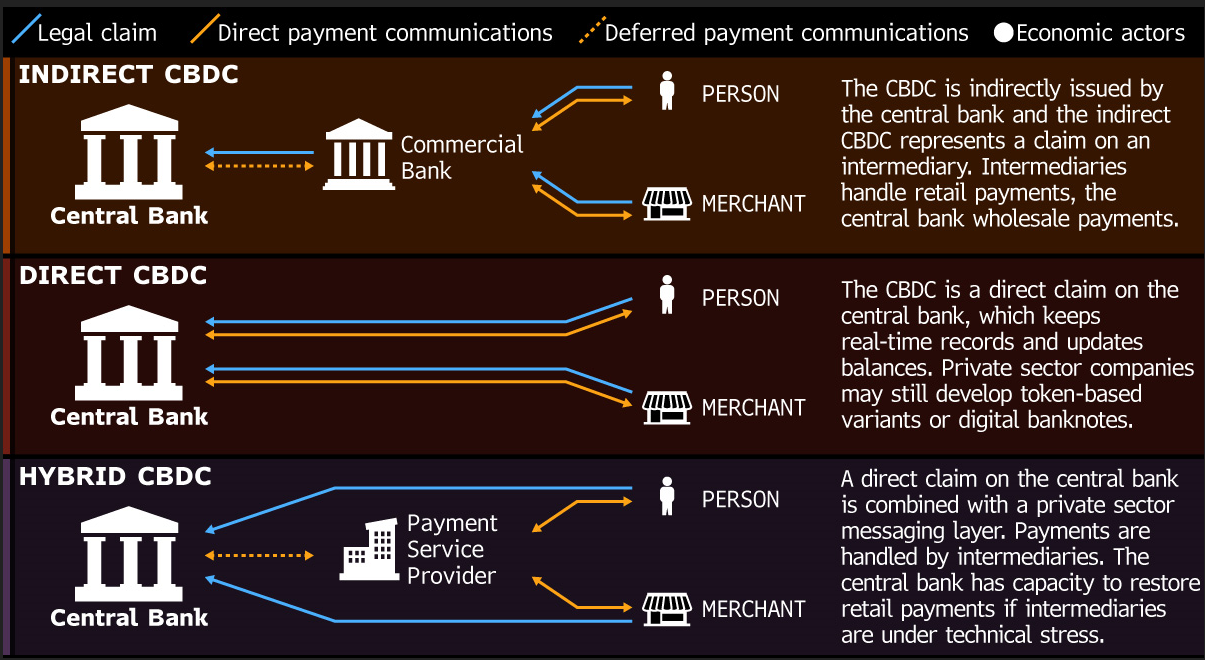

The emergence of money digitalization

The value of CBCDs is associated with the issuing country’s official currency. Physical currency remains widely used across the globe. However, people are still beginning to move away from cash and embrace digital financial transactions.

This was particularly seen with the COVID-19 pandemic, where hygiene concerns and cash shortages limited physical currency exchanges. According to McKinsey, financial institutions and banks across the world process more transactions digitally than they do in their physical branches. There’s no denying there have been digital disruptions in the financial services sector over the last number of years.

These disruptions can be credited to the likes of blockchain technology and cryptocurrencies. Central bank digital currencies fall under this umbrella, and central banks are starting to recognize this as the world opts for all things digital. Central bank digital currencies are not so different to stablecoins. The main difference between the two is that CBCDs are both state-operated and issued.

How a CBDC could work | Source: Bloomberg

There are many reasons banks and financial institutions worldwide have turned their attention to CBCDs. UK Finance reports cash has fallen from 62 percent of payments in 2006 to 15 percent in 2021 in the United Kingdom. The decrease in physical cash transactions is reflected across the globe too, with much discussion about whether cash will survive and whether we will move to a cashless future.

Additionally, there is a growing interest in privately issued digital assets. CBDCs also give central banks a bright new opportunity to lead strategy conversations on cash use cases in public forums. Many central banks are also looking to build greater local governance over increasingly global payment systems. Therefore, the banks view CBDCs as a potential stabilizing anchor for local digital payment systems.

Benefits of CBCDs

CBCDs can be built for both wholesale and retail payments. A wholesale CBDC refers to an entirely new infrastructure for interbank settlements, while a retail CBDC involves a digital version of cash. Central banks have trialled both with a focus, particularly on low-cost, fast payments.

One of the most significant advantages of CBCDs is they can offer a reliable and secure means of digital payment and remittance. They can be used for offline and online transactions. CBCDs can enhance payment accessibility and efficiency. They can also be integrated into existing payment systems. Not to mention, CBCDs can be utilized to facilitate cross-border payments.

These transactions can be made without the need for intermediaries like payment processors or banks. Cross-border payments are already a significant challenge for banks concerning fiat money. It’s for these reasons that numerous central banks across the globe have already begun to experiment with CBDCs to explore their economic potential.

CBDCs can also offer financial inclusion for those currently underbanked or unbanked. They can make it easier for people to access financial services and engage in the digital economy due to being a digital alternative to cash. This is a big issue CBDCs can challenge, which will be particularly monumental for people in developing nations where traditional banking services are limited.

They can also curb the demand for physical cash. CBDCs can reduce the need for cash transportation and handling, which can pose security risks and be expensive. This would help minimize theft and counterfeiting, two significant issues associated with physical cash. CBDCs offer increased transparency and security, too.

They do this by offering strong authentication and encryption protocols that can assist in preventing cyberattacks and fraud. CBDCs are also an emerging tool for implementing monetary policy. They can offer central banks real-time data concerning the state of the economy, helping them make better-informed policy decisions.

Disadvantages of CBDCs

Despite the many benefits offered by CBDCs, they do have some drawbacks. One critical thing to keep in mind is that the currently available technology will not be able to cater to large volumes of citizens using CBDCs. To put that into perspective, the daily volume of retail CBDCs is expected to be higher than 100,000,000 transactions.

While CBDCs have the potential to prevent cyberattacks, they may also be vulnerable to them due to the limitations of cryptography. This could lead to financial losses and ultimately disrupt the financial system. It should also be noted that CBDCs still require fiat-to-fiat conversation for cross-border transitions. CBDCs use a single centralized network, so if this goes down, the digital currency will no longer be usable.

There is also a risk concerning national cash monopolies. Central banks fear that CBCDs could reduce the monopoly of sovereign money, compromising their ability to maintain financial and monetary stability. In terms of other drawbacks, CBDCs could cause increased surveillance of financial transactions. This is a problem because it could raise both security and privacy concerns.

Another thing to keep in mind is that the implementation of CBDCs could be a complex and costly process. In other words, implementing CBDCs will require an understanding of both encryption processes and blockchain technologies. They may also require new legal frameworks and regulations, which will take some time to develop.

There could also be some risks associated with integrating CBDCs into existing payment systems. It is also uncertain what impact CBDCs could have on the banking sector. Some worry they could have a negative impact, and banks could face increased competition from them, resulting in a reduction in the availability of credit and a decline in their profits.

There are also concerns that CBDCs could negatively affect monetary policy. The use of CBDCs could hinder the ability of central banks to implement monetary policy. This would cause economic problems like increased inflation. It is a completely new economic approach, and so, there may be unforeseen consequences for individuals and businesses.

How can we make CBDCs successful?

The interest in CBDCs is there, but the drawbacks mean there are several risks. For CBDCs to be successfully integrated, we need to draw on their areas of expertise within the payments ecosystem.

This means establishing a design whereby central banks can issue CBDCs to payment service providers, fintechs, and commercial banks. By distributing CBDCs to these various providers, they will be responsible for offering the digital currency to merchants and consumers.

It is vital we establish a model whereby compliance checks like anti-money laundering and know your customer (KYC) are prioritized. By assessing the digital currencies currently in circulation, financial institutions can develop strategies, products, and infrastructure that support the future of CBCDs.

Ultimately, for any technology to achieve widespread adoption, it must work for individuals in a range of contexts and locales. Financial institutions need to invest in digital currency education, analyze various use cases, and create their digital currency strategy.

The future of CBCDs

Many countries and financial institutions are turning their attention to CBDCs with the belief that they could be the future of payments. The interest in CBDCs is justified as they do offer many benefits compared to traditional cash and cryptocurrencies. However, they still do have several drawbacks that pose serious risks to citizens and the banking sector.

CBCDs will likely continue to gain traction, and they have huge potential. In saying that, we must not forget to pay attention to their disadvantages and work to make them successful and risk-free.