Tokenization of real estate: evaluating the promise of securitization | Opinion

Disclosure: The views and opinions expressed here belong solely to the author and do not represent the views and opinions of crypto.news’ editorial.

As it gained traction in the crypto industry, real estate tokenization is classified as a security in most jurisdictions with developed financial regulations, such as the United States, European Union, United Kingdom, Australia, and others. In this article, I examine the limitations of tokenization-securitization and explore why the concept of tokenization should aim to digitize property rights instead, penetrating the very heart of land registries. In my previous article, I outlined the idea of the “title token” and the concept of the next-generation land registry—blockchain estate registry. Now, let us scrutinize the promise of securitization to illustrate why, without redesigning the system, the digital economy will not progress.

Securitization explained

Traditionally, real estate has been viewed as a valuable asset class but has presented challenges for smaller investors due to its illiquid nature and substantial upfront investment requirements. It is commonly believed that blockchain technology offers a promising solution through the tokenization of real estate. This widespread interpretation involves converting real-world assets into digital tokens tradable on a blockchain, thereby subdividing the asset into smaller, more manageable units. This approach purportedly makes investment more accessible and enhances the liquidity of real estate, as these tokens can be easily traded on secondary markets.

However, while such tokenization has garnered attention, a critical examination of its limitations is essential. The following scrutiny reveals the inadequacies of this model and underscores why a thorough redesign of the land system is imperative to ensure meaningful progress.

Essentially, such tokenization represents securitization. A typical scheme authorized by a financial regulator involves the creation of a special purpose vehicle (SPV), e.g., a corporation or a trust, where tokens represent shares or units, respectively. Rarely, when tokens represent neither of these, such security can fall under a larger category of an “investment product” or “managed investment scheme” found in regulations of many countries since the case of SEC vs Howey in the U.S. in 1946.

Economically, such a security would generally be understood as someone’s promise in exchange for cash to perform some economic venture that might result in profits. Thus, there are two sides to this deal: someone who promises something and the one who invests money. To complete this picture, there can be a secondary market where such securities are traded between those who hold them and those who want to acquire them.

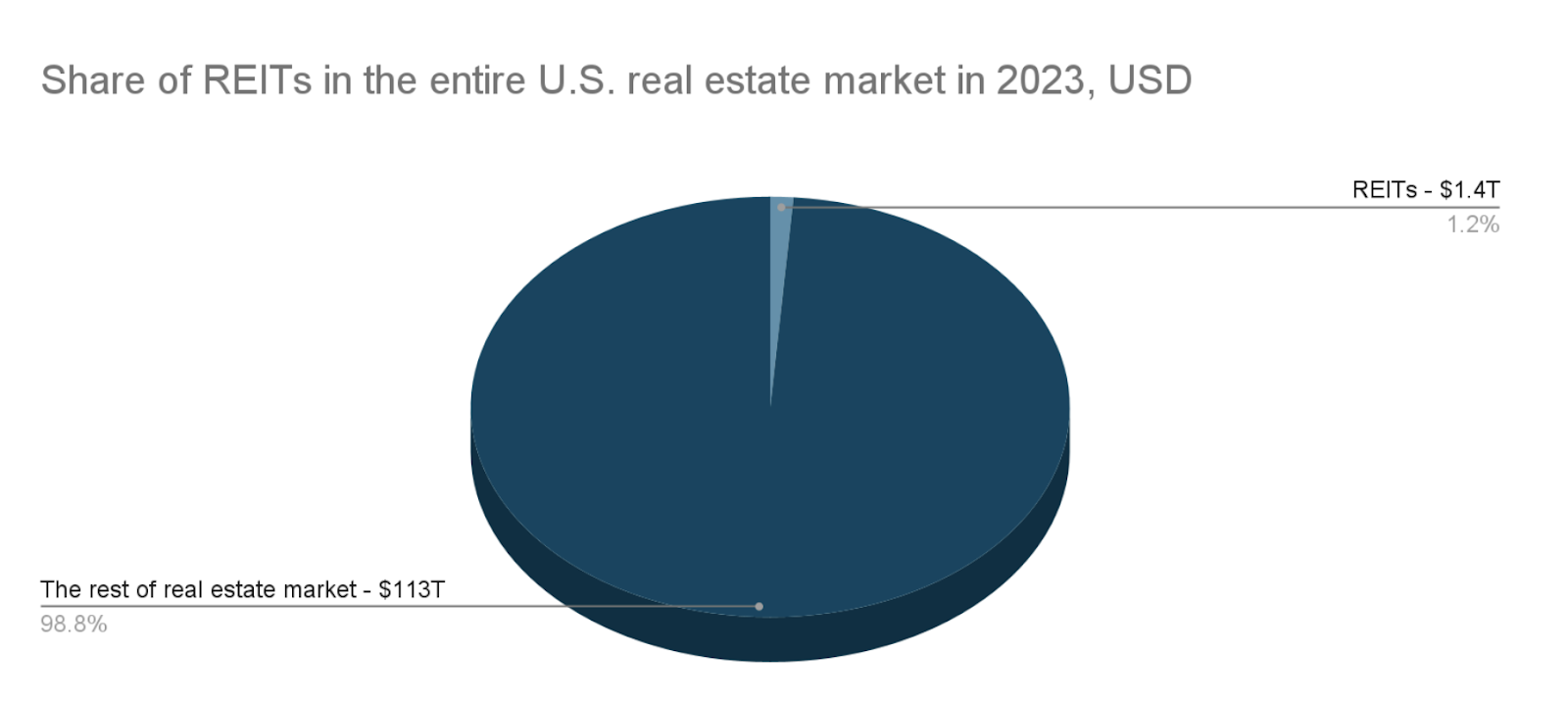

When it comes to the economy around real estate, traditionally securitized property represents a small fraction of the overall property market. For instance, as of 2023, the market capitalization of US publicly traded real estate investment trusts (REITs) was approximately $1.4 trillion, which is 1.3% of the whole US real estate value, estimated at $113 trillion.

This disparity highlights that securitized real estate forms only a minor segment of the broader property market. The limitation arises from the legal nature of such relations. Security is an economic interest in someone’s property (a promise secured with a legal instrument). The one who holds the security is not the property owner. The security holder does not enjoy the whole bundle of legal rights; hence, its economic application is also limited.

Security token vs. Title token: A real estate security token represents the holder’s economic interest in someone else’s property. A title token is the actual record of the property right.

Why #tothemoon won’t happen

Starting from the first wave of tokenization—also known as the initial coin offering boom—in 2016-2017, there has been unreasonable excitement around real estate tokenization, which aligns with the hype that is overall present in the crypto industry. Tokenization is associated with the potential for high profits, which are made on market bubbles.

Tokenization of real estate is advocated as a way to increase the liquidity of real property. It is usually explained that digital technology along with fractionalization will reduce the barriers and make this investment more attractive. It will, no doubt, but having real estate as the underlying asset projects the behavior of the underlying asset.

Prices on real estate are not the same as company stock markets, where business expansion and innovation can make company shares skyrocket. Usually, real estate doesn’t dramatically fluctuate; moreover, it is unlikely that one building will rapidly increase in price while the rest around it stay the same. Normally, the real property market moves all in one trend, with some minor discrepancies from region to region.

REITs and real property tokens

It is reasonable to interpolate publicly listed real estate investment trusts (REITs). Investment trusts democratize investments in real estate by reducing barriers, as these are shares of companies that own real property traded on exchanges.

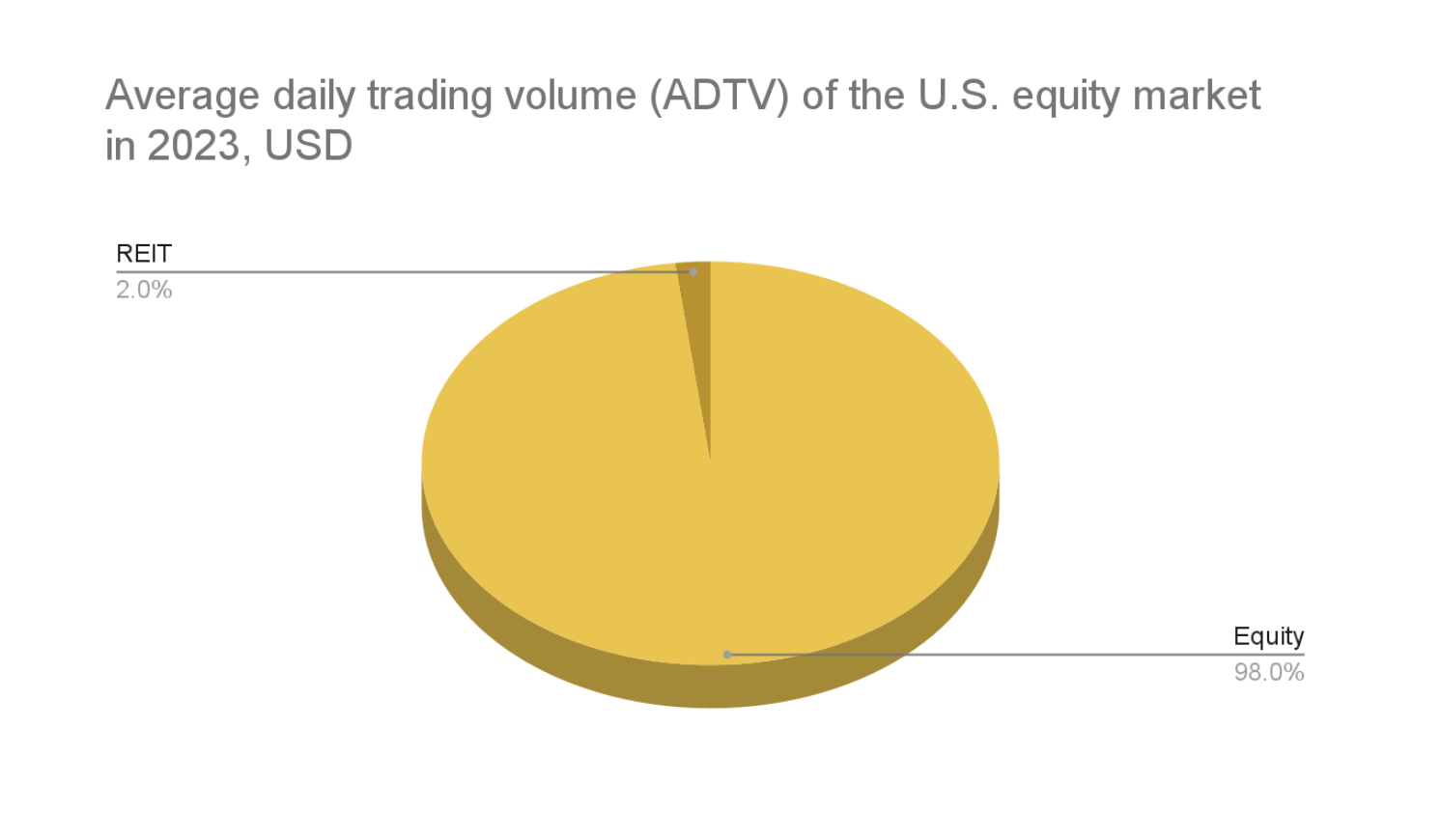

It is evident that daily dollar volumes on REIT markets are much lower than on major stock exchanges. The average daily trading volume (ADTV) of the U.S. equity market exceeded $500 billion in 2023, while publicly-traded REITs often see volumes in the range of $10 billion.

Additionally, REIT markets exhibit lower volatility compared to the broader stock market. This stability stems from the nature of their underlying assets—real estate—which typically do not experience dramatic short-term price swings. Most importantly, public REITs go along with the general trend in the real estate market. The performance of REITs often reflects the broader trends in the real estate market because both are influenced by similar economic factors such as interest rates, economic growth, and property values.

So, the overall excitement about real estate tokenization looks more irrational. It is unreasonable to expect that tokenized property will make substantial gains, while, for example, the rest of the real estate market is stagnating. Nevertheless, with the digitalization of finance, it is reasonable to expect a reduction in transaction costs. Web3 and other digital technologies can make security markets more transparent and accountable, rendering some bureaucratic procedures redundant and obsolete. Thus, the advent of innovations can make the REIT market more efficient under the condition that the government reduces red tape to unleash the potential of digital technologies.

Now, facts and some concluding thoughts

Finally, let us explore some empirical evidence that supports this discussion. STM (Stomarket.com) is a popular resource in the world of tokenized real-world assets (RWAs). Similar to Coinmarketcap.com, it consolidates tokens, their capitalization, volumes, and other essential market data.

A closer examination shows how much smaller the tokenized RWA market is compared to the cryptocurrency market. STM’s capitalization of listed 465 ‘Real Property’ tokens is $226 million with only $1.7 million of trade volume per day. For comparison, Coinmarketcap’s list capitalization is $2.3 trillion, with $72.6 billion of trade volume per day of over 8,000 coins and tokens listed on the website (as of 14 May 2024). Deloitte analysis indicates more optimistic figures—$16.4 billion capitalization in 2022, according to their research, which is still 140 times smaller than Coinmarketcap’s list.

In summary, securitization is no revolution, and speculative excitement around the tokenization of real estate markets is far-fetched. Blockchain and other web3 technologies can make the securitization of real estate more efficient if introduced with more progressive regulations. However, securitized property constitutes just a small portion of the whole real estate market, so bringing efficiencies to this small segment does not make much of a difference.

All property rights, titles, and legal interests, in fact, are locked in government registries—old-fashioned land registries with paper-based transactions and bureaucratic registry and titling services. With web3 technologies, economic relations can become transboundary, online, instant, and peer-to-peer. Programmable relations reduce the need for intermediaries, i.e., agents, lawyers, notaries, conveyancers, and other registrars.

The old registry constitutes a bottleneck for the future of the digital economy as all this potential efficiency bumps up against the old-fashioned sluggish system. Government inertia to improve the system, i.e., automate and digitize, stifles the further evolution of the economy. In fact, the appearance of traditionally securitized and tokenized real property is a kind of response to that inefficiency. Though, as it was shown, it has a marginal effect that does not change the whole picture.