A taxing year for digital assets begins | Opinion

Disclosure: The views and opinions expressed here belong solely to the author and do not represent the views and opinions of crypto.news’ editorial.

A bull market for digital assets is on the horizon for 2024. With abundant investment opportunities abound digital asset investors should be aware that the IRS announced that during 2024, it would focus on compliance initiatives associated with digital assets, FBAR, high-income and high-wealth taxpayers.

The veil on the identity of Satoshi Nakamoto, the author of Bitcoin’s White Paper that proposed the blockchain-based decentralized cryptocurrency, still has not been lifted. This “‘identity issue,’ namely whether Dr. Craig Wright is the pseudonymous ‘Satoshi Nakamoto,’ i.e., the person who created Bitcoin in 2009” or not, according to High Court Judge John Mellor, is still being litigated in the United Kingdom with the support of Bitcoin Legal Defense Fund set up by Block CEO Jack Dorsey. As Jack explained:

“The Bitcoin Legal Defense Fund is a nonprofit entity that aims to minimize legal headaches that discourage software developers from actively developing Bitcoin and related projects such as the Lightning Network, Bitcoin privacy protocols, and the like.”

Unfortunately, the self-proclaimed inventor of Bitcoin, Dr. Craig Wright, is only one of many to claim to be Satoshi Nakamoto, according to the article “The Faketoshi,” authored by Arthur van Pelt.

Adding layers to Satoshi’s identity mystery is a Binance wallet sending approximately $1.2 million worth of Bitcoin (BTC) to Satoshi’s Genesis wallet on January 5, 2024, which coincided with Judge Mellor’s order to Dr. Craig to pay over $1M to the court and was two days after BTC’s 15th birthday.

The mist around Dr. Craig’s ‘identity issue’ is expected to lift Judge Mellor said, “By 4 pm on January 18, 2024, [when] Dr. Wright and COPA [Crypto Open Patent Alliance] shall exchange and shall serve on the Developer Defendants expert reports on (a) forensic document analysis in respect of the Additional Documents,—[95 documents dating back to 2007]—stored on the Samsung Drive, and the BDO Drive; and (b) LaTeX software.” Within the later development, the case is expected to commence on February 5, 2024, according to the latest release published on the COPA website.

Once the identity of Satoshi is known, if this person is a US person with an estimated BTC wealth of $40 billion, the US taxpayer is expected to file Form 8300 with the IRS within 15 days after receiving the digital assets of $1.2M in BTC received since effective January 1, 2024, any crypto transaction over $10,000 must be electronically (if they are required to file certain other information returns electronically) reported when regulations are finalized. Noncompliance with Form 8300 results in subjecting taxpayers to civil and criminal penalties.

Bad actors out of the way

While the “real” author of the Bitcoin White Paper continues to be debated in the United Kingdom’s court system, the digital asset industry went through a cleansing of bad actors in the US during 2023. The world’s largest crypto exchange, Binance, and its CEO pleaded guilty to federal charges. They agreed to pay over $4B to resolve the Justice Department’s investigation into the Bank Secrecy Act violations, failure to register as a money-transmitting business, and the International Emergency Economic Powers Act (IEEPA).

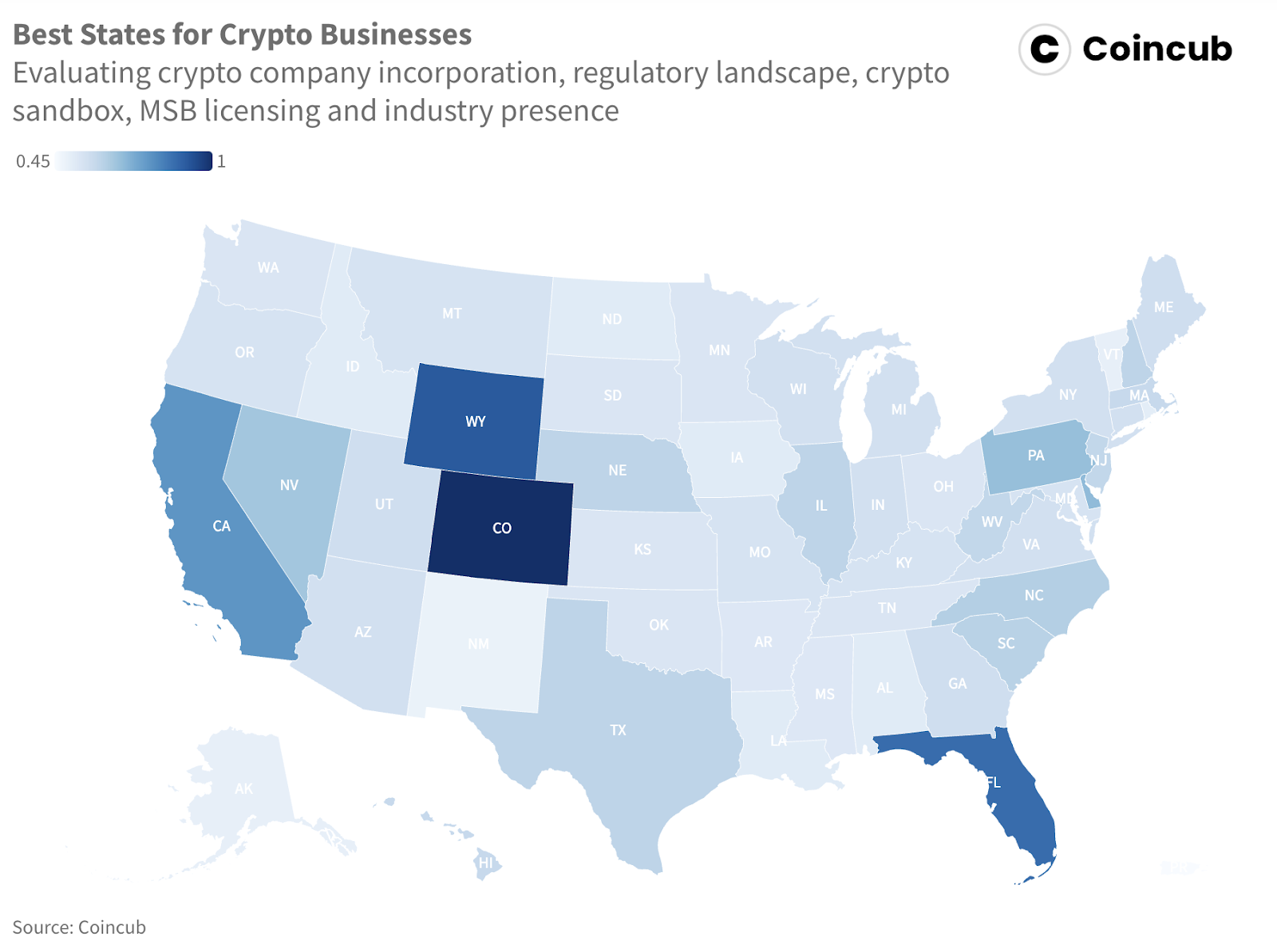

Binance, Coinbase, Terraform Labs, and others also faced action by the SEC for operating unregistered securities exchanges, which are still ongoing. As Sergiu Hamza, CEO of Coincub, a company that has prepared reports on the US money services business (MSB) and global Virtual or Digital Asset Service Providers (VASPs), explained to me in a private interview:

“In 2023, the US experienced significant regulatory shifts, particularly in response to the FTX collapse, which was followed by five crypto-friendly bank failures. The Biden administration’s ‘regulation by enforcement’ strategy shaped the federal landscape, spearheaded by Gary Gensler and the SEC. Amidst this, states like Colorado stood out as beacons for the crypto industry, accounting for 33% of all U.S. crypto businesses. This success is primarily attributed to forward-thinking measures such as Colorado’s ‘Digital Token Act’ and key initiatives like ETH Denver, all nurtured under Governor Jared Polis’ vision.”

Best states for crypto businesses | Source: Coincub

North American investors, money managers, and even CBOE Digital president John Palmer are confident that a new wave of institutional and pension fund investment will follow spot Bitcoin ETF approvals. Already, several spot BTC exchange-traded fund (ETF) applicants—such as Vaneck, Valkyrie, Grayscale Investments, Fidelity, BlackRock, and Bitwise—filed to register their funds as securities with the US Securities and Exchange Commission with an approval deadline of January 10, 2024. The first spot BTC ETF application was made by Cameron and Tyler Winklevoss, filed on July 1, 2013, with the SEC a decade ago. As Sergiu Hamza commented in a private interview:

“As we move into 2024, the launch of Bitcoin ETFs marks a significant milestone, particularly for Wall Street. This development enhances Bitcoin’s appeal and credibility, heralding a market ripe for expanded investment and engagement from political and financial sectors, potentially catalyzing the next chapter in Bitcoin’s growth.”

After a bear market in 2022, Bitcoin’s value surged 160% during 2023 and continues on an upward trend. William Quigley, co-founder of Tether and WAX Blockchain, said to me, “Unlike previous crypto bull market years, crypto-focused investment funds have large reserves of investable cash. This is a positive factor in driving a crypto bull market.” He continues:

“There are many more investment funds operating in 2024, with much more crypto investing experience. ETFs are a mixed bag for crypto enthusiasts. While they provide a new way for institutional investors to acquire Bitcoin, they also provide an easy way for those investors to short Bitcoin. This might cancel out any sustained buying support for bitcoin in 2024.”

BRICS doubled in size

In 2018, Russia took the lead in proposing a multinational stablecoin backed by commodities with the Eurasian Economic Union, or EAEU, and BRICS countries. At the beginning of 2024, five more countries joined BRICS, including Saudi Arabia, the United Arab Emirates (with a joint coin initiative, Aber), Iran, Egypt, and Ethiopia. At the beginning of the year, Russia was passed the baton of the BRICS chairmanship.

BRICS member countries plan to launch a common currency for their organization that could be a multinational digital currency backed by a basket of assets or gold. BricsTether has already launched a stablecoin backed by a basket of assets, providing greater stability and predictability than traditional cryptocurrencies.

However, China’s top legal watchdog recently clamped down on Tether’s use by declaring that exchanging local currency for foreign ones using Tether-USDT stablecoin or providing technical support for exchange services for such transactions is unlawful.

Furthermore, an order from Judge Jed Rakoff in the US District Court for the Southern District of New York, who granted summary judgment for the SEC, stated that stablecoins LUNA, UST, and MIR are securities.

Accordingly, BricsThether or BRICS-issued multinational stablecoin could be subject to SEC oversight as a security. US BricsTether or BRICS stablecoin holders may be subject to FBAR and Form 8938 Foreign Account Tax Compliance Act (FATCA) reporting requirements.

With abundant investment opportunities abound digital asset investors should be aware that the IRS announced that in 2024, it would focus on compliance initiatives associated with digital assets, FBAR, high-income and high-wealth taxpayers. Noncompliance with FBAR FinCen Form 114 and Form 8938 subject taxpayers to severe civil and criminal penalties, potentially in excess of the unreported foreign assets. For institutions, noncompliance can result in exclusion from access to US markets.